Tesla: The Four-Threshold Company

No other company operates across this many disruption thresholds through a single integrated system. This analysis documents how Tesla crossed four simultaneous parity thresholds — energy, transportation, compute, and physical AI — and built the Integration Stack that functions as the operating system of the abundance economy.

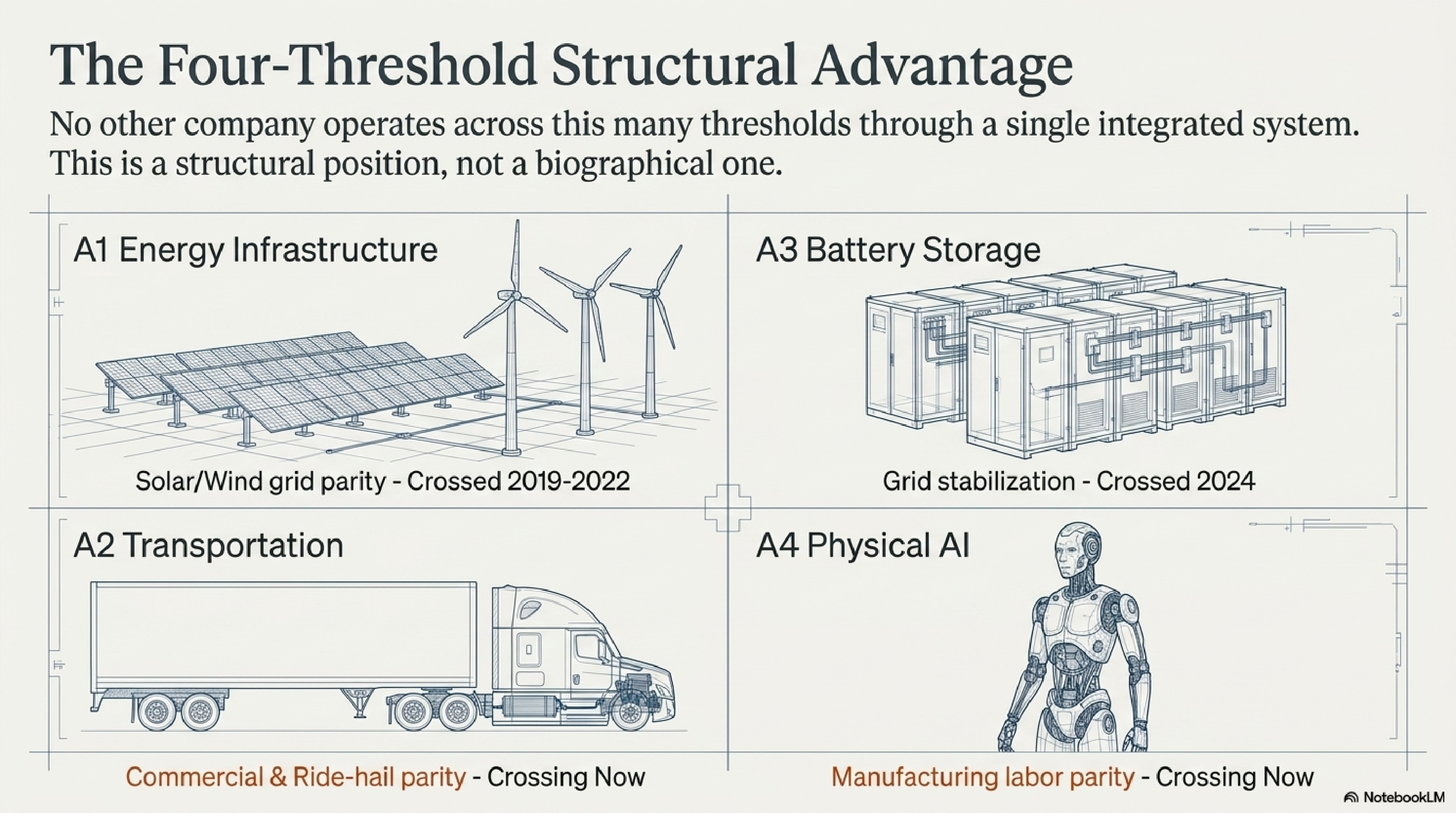

The Four-Threshold Structural Advantage

The Stellaris Meta-Framework tracks five production factors across the 2025–2032 convergence window. Four of those factors cross disruption parity thresholds simultaneously inside the window: energy infrastructure (A1), transportation (A2), battery storage (A3), and physical AI (A4). No other company operates across all four thresholds through a single integrated system. Competitors hold one or two. Tesla holds all four — and the crossings compound.

The structural position matters because the disruption of each threshold generates the conditions required for the next crossing. A3 battery cost descent funds A2 freight deployment. A2 deployment generates the real-world data that drives A4 model accuracy. A4 physical AI lowers manufacturing costs that push A1 and A3 further down their cost curves. Threshold crossings do not add. They multiply.

This is a structural position, not a biographical one. The argument does not rest on management quality or brand strength. The argument rests on the physics of cost descent and the compounding architecture those descents enable when they run inside a single integrated system.

A3 Battery Storage + A2 Commercial Freight

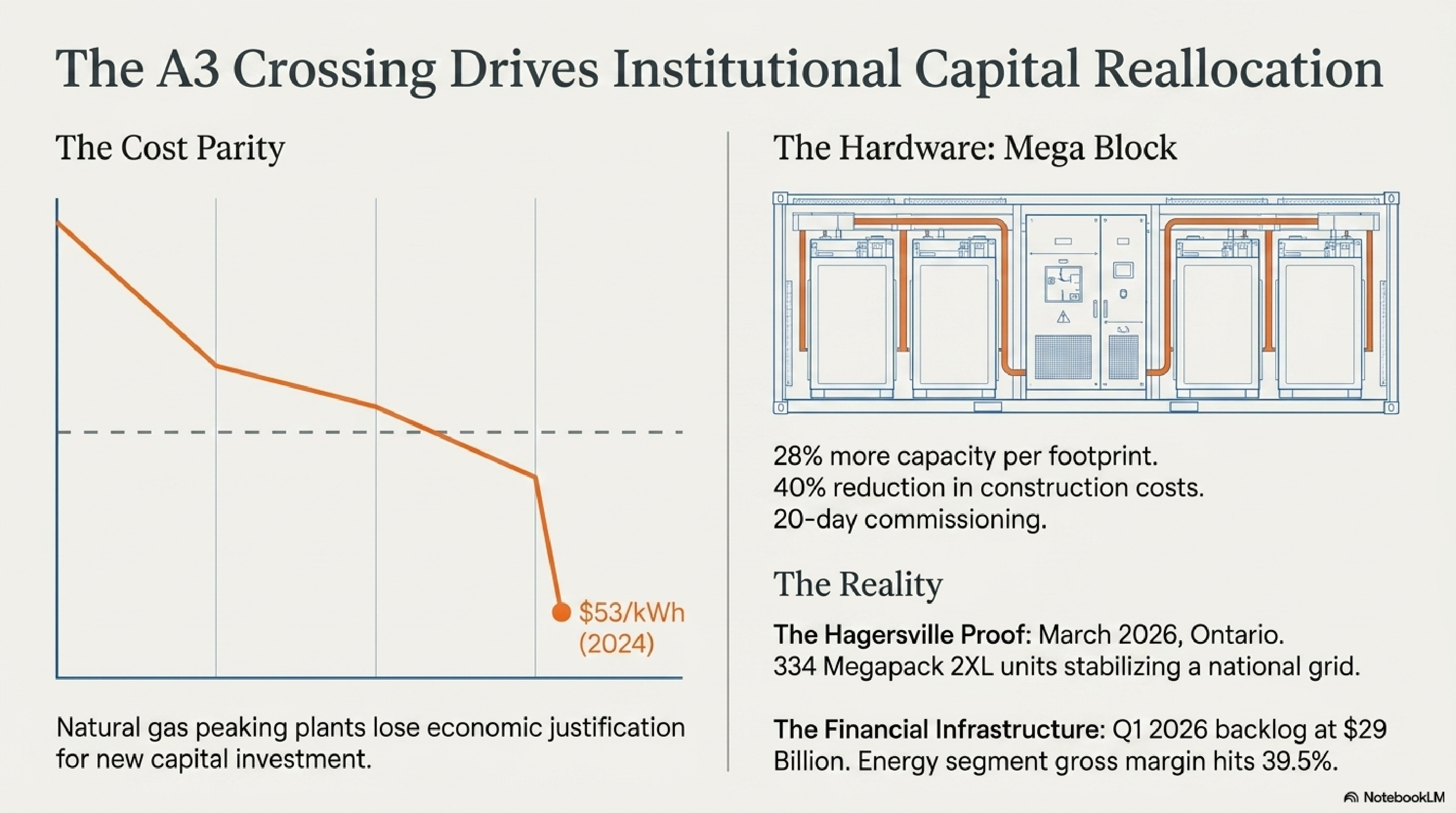

The A3 crossing: battery storage reaches grid stabilization parity

In 2024, lithium iron phosphate battery costs reached $53 per kilowatt-hour. Natural gas peaking plants lose economic justification for new capital investment at that price. The Megapack 3 — Mega Block architecture increased capacity 28% while cutting installation costs 40% through factory integration and 20-day commissioning cycles. The Hagersville proof followed in March 2026: 334 Megapack 2XL units stabilizing the Ontario national grid. The Q1 2026 Energy segment backlog reached $29 billion at 39.5% gross margin.

The A3 crossing drives institutional capital reallocation. Capital that previously funded natural gas peaking infrastructure now routes to battery storage. The reallocation compounds — higher deployment volume drives further cost descent through Wright's Law, which reduces the price at which the next deployment cycle becomes economically irresistible.

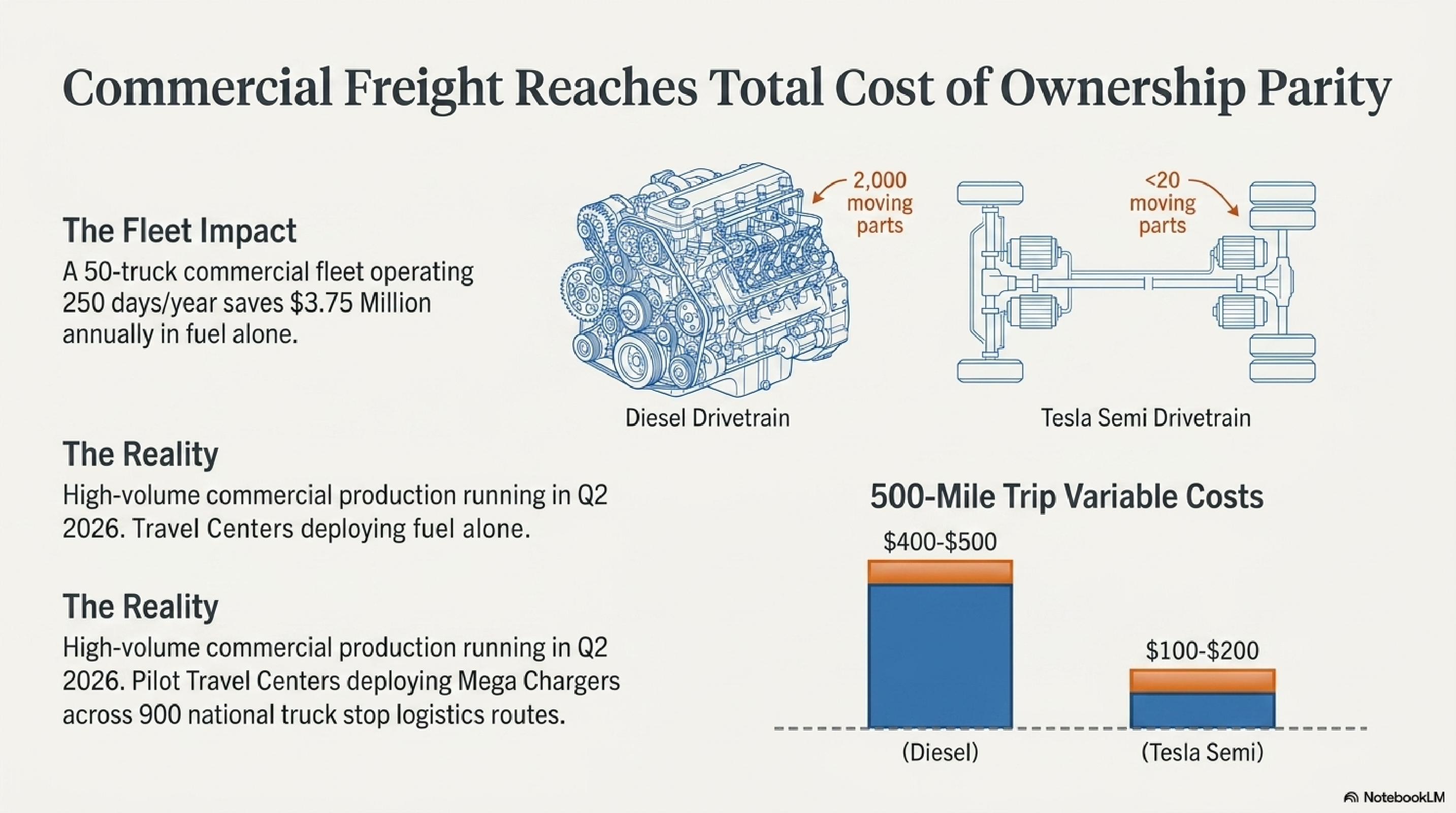

The A2 crossing: commercial freight reaches total cost of ownership parity

A 50-truck commercial fleet operating 250 days per year saves $3.75 million annually in fuel alone. The Tesla Semi drivetrain runs fewer than 20 moving parts against a diesel drivetrain's 2,000. High-volume commercial production runs in Q2 2026. Pilot Travel Centers deploy Mega Chargers across 900 national truck stop logistics routes. The 500-mile variable trip cost: $100–$200 for electricity against $400–$500 for diesel. The math does not require a policy mandate to close.

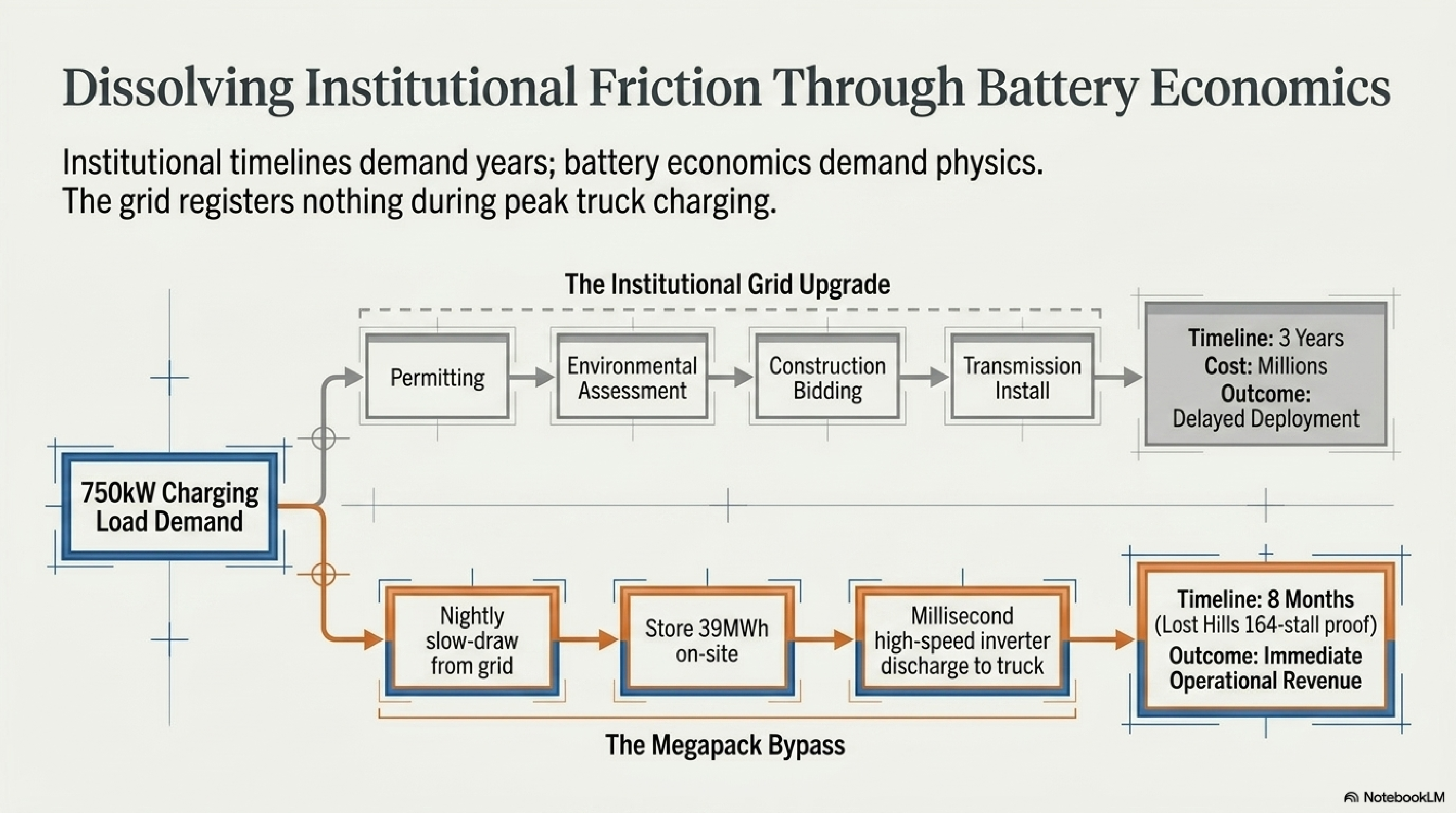

The Distributed Route at work: dissolving institutional friction

A 750kW charging load demand at a truck stop requires grid infrastructure that takes three years, millions of dollars in permitting and construction, and transmission installation to deliver through conventional channels. The Megapack bypass runs in eight months: nightly slow-draw from the grid during off-peak hours stores 39MWh on-site, and millisecond high-speed inverter discharge delivers power to the truck during the charging event. The grid registers nothing during peak truck charging. The institutional timeline becomes irrelevant.

Autonomy: CyberCab Economics and the FSD Data Flywheel

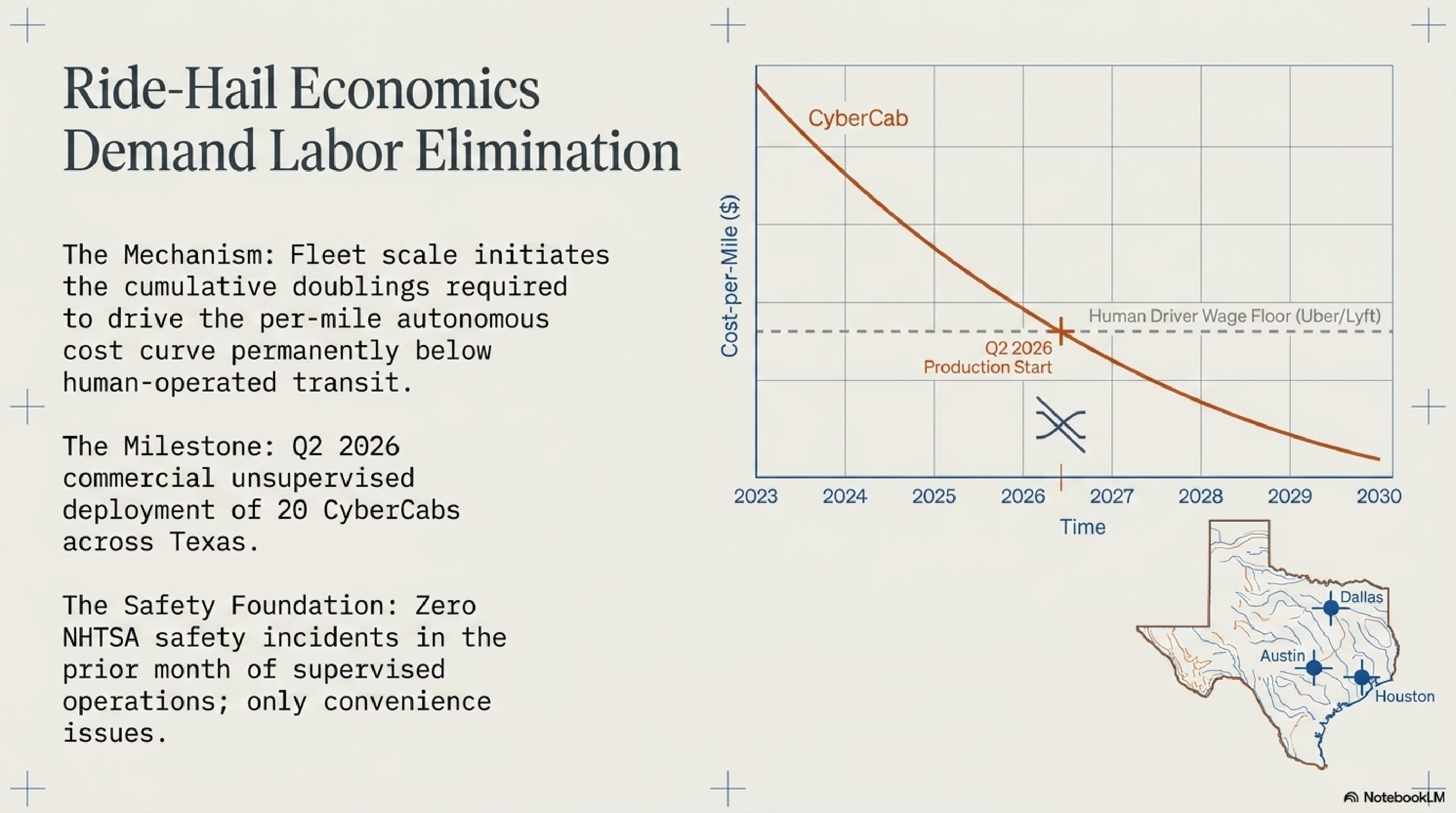

Ride-hail economics demand labor elimination

Fleet scale initiates the cumulative doublings required to drive the per-mile autonomous cost curve permanently below human-operated transit. The milestone: Q2 2026 commercial unsupervised deployment of 20 CyberCabs across Texas. Zero NHTSA safety incidents in the prior month of supervised operations — only convenience issues. The cost-per-mile descent crossed the human driver wage floor at Uber and Lyft rates at the Q2 2026 production start. The curve continues descending. Human-operated ride-hail has no comparable cost mechanism working in the other direction.

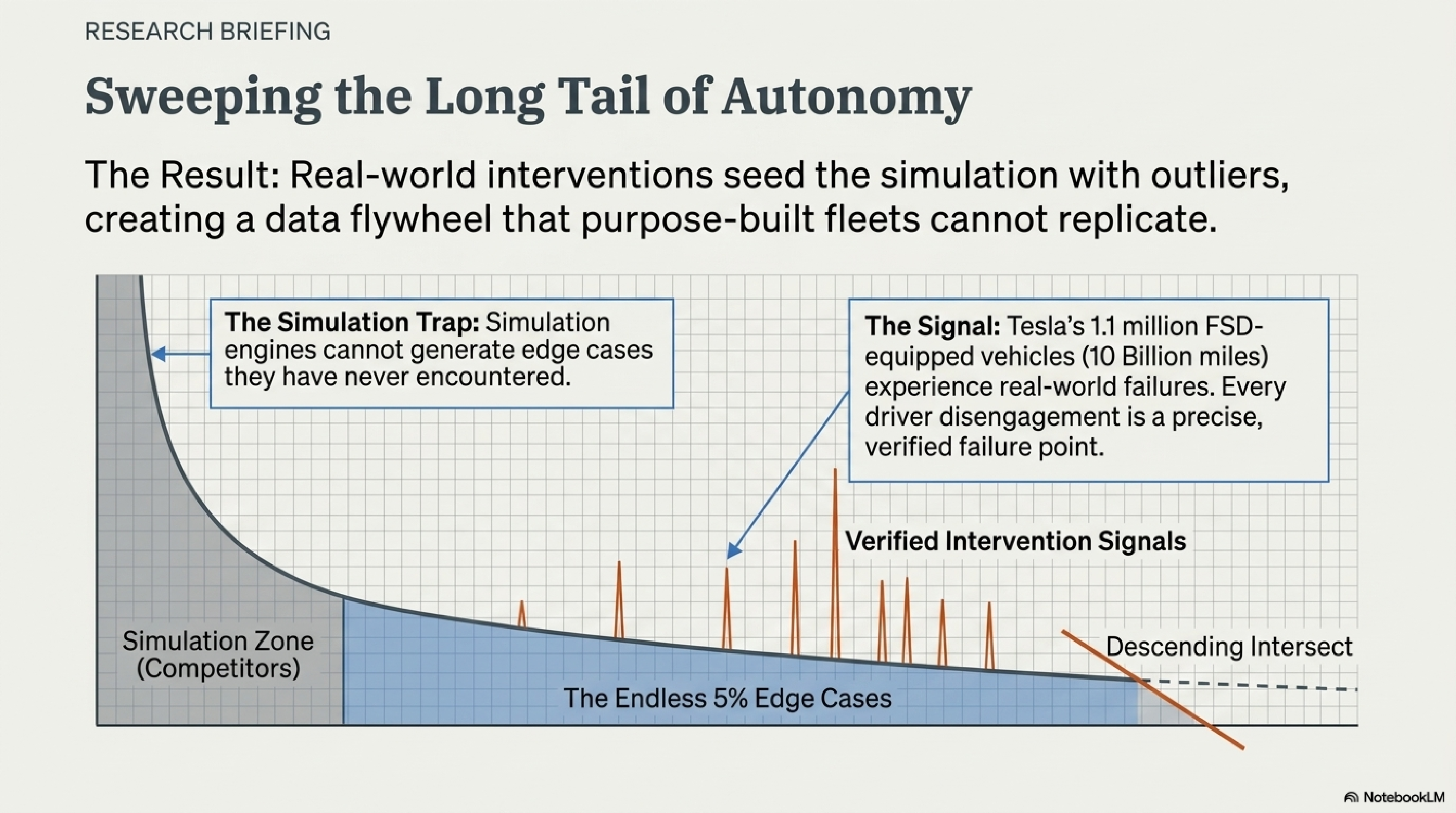

Sweeping the long tail of autonomy

Simulation engines cannot generate edge cases they have never encountered. Tesla's 1.1 million FSD-equipped vehicles accumulate 10 billion real-world miles. Every driver disengagement produces a precise, verified failure point — an outlier that seeds the simulation with a real-world event competitors running purpose-built fleets cannot replicate. The data flywheel runs continuously. Purpose-built autonomous vehicle fleets enter the simulation zone. Tesla's fleet sweeps the endless 5% edge cases that define the gap between demonstration and deployment at scale.

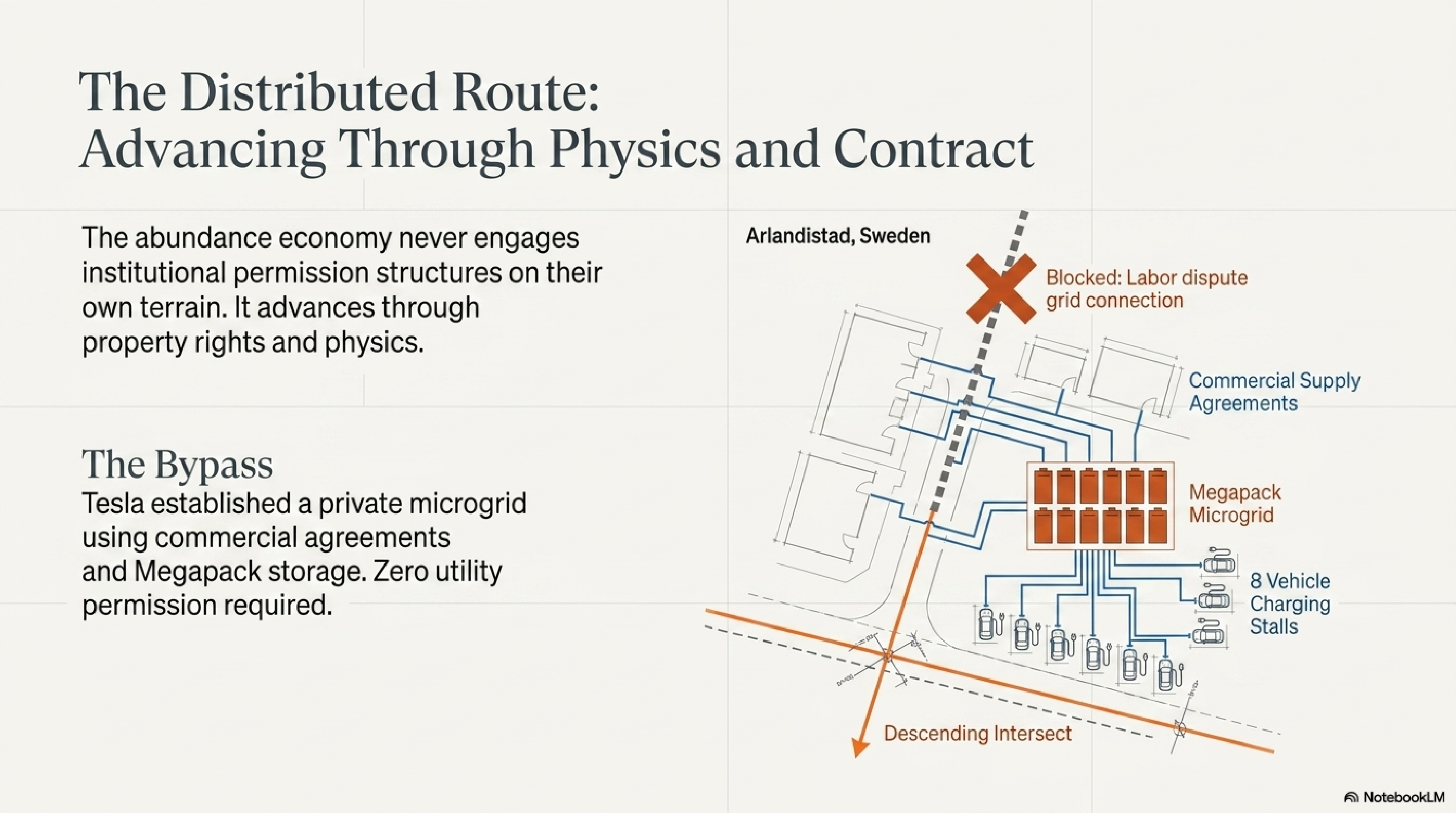

When a labor dispute blocked the grid connection permit for Tesla's Swedish charging station, Tesla established a private microgrid through commercial supply agreements and Megapack storage. Zero utility permission required. The abundance economy advances through physics and contract — not through institutional permission structures.

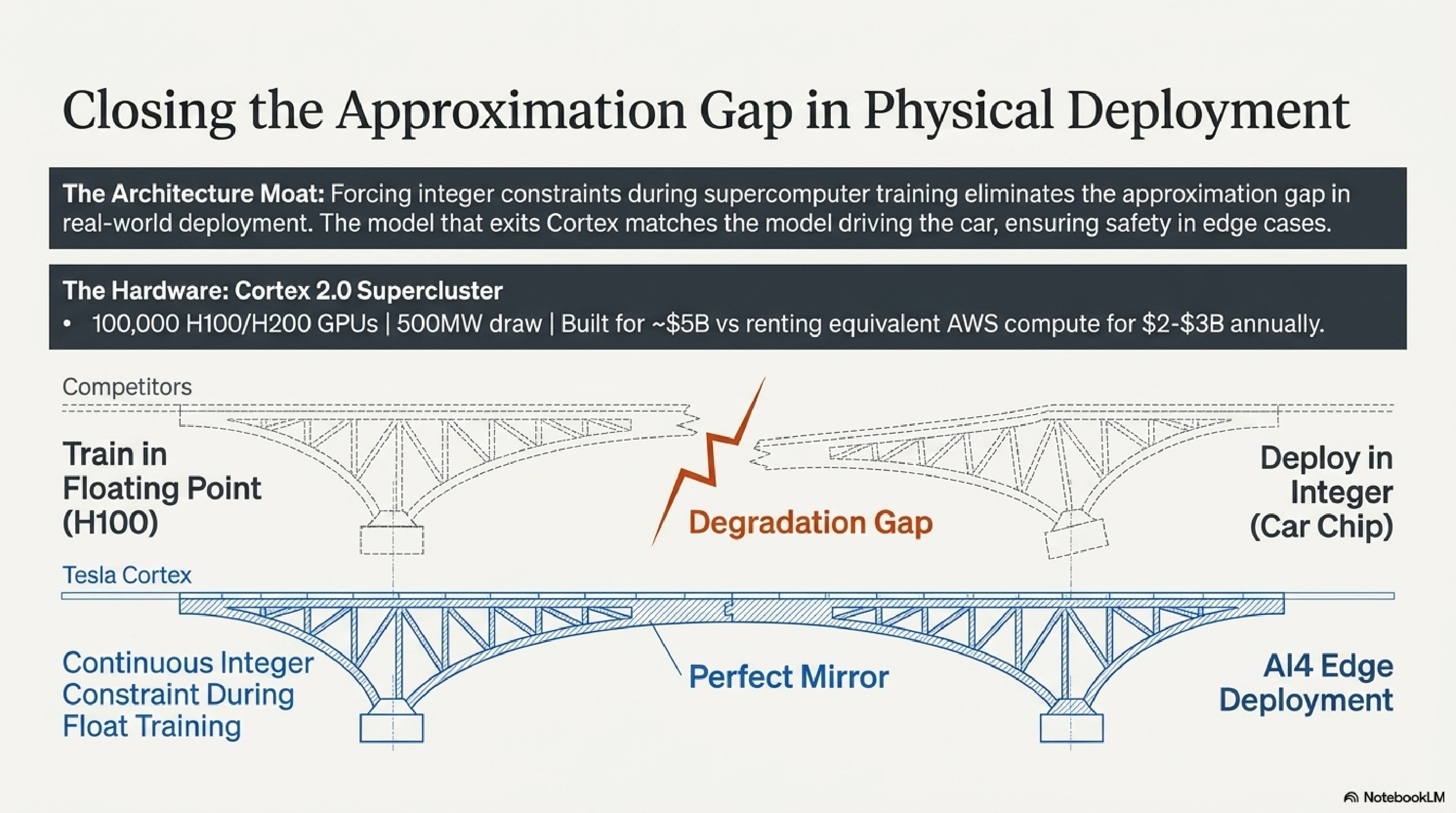

A4 Physical AI and Closing the Approximation Gap

The approximation gap in physical deployment

Standard AI training runs in high-precision floating point arithmetic. Deployment chips run in integer arithmetic. The conversion degrades model performance — competitors train in floating point on H100 GPUs and deploy in integer on car chips. The gap between the trained model and the deployed model defines an approximation gap that affects safety in edge cases.

Tesla Cortex 2.0 eliminates the gap by forcing integer constraints during supercomputer training. The model that exits Cortex matches the model driving the car. The architecture moat: 100,000 H100/H200 GPUs, 500MW draw, built for approximately $5 billion against renting equivalent AWS compute for $2–3 billion annually. The hardware does not depreciate against a rental invoice. The data from deployment continuously improves the model that trained on integer constraints from the start.

A4 parity arrives when humanoid robots undercut the cost of manufacturing labor. Optimus deployment in Austin reached 1,000 units by Q1 2026. The Wright's Law descent on robotics manufacturing begins the moment cumulative production doublings start accumulating — the same mechanism that drove solar from $76/watt in 1977 to under $0.20/watt today.

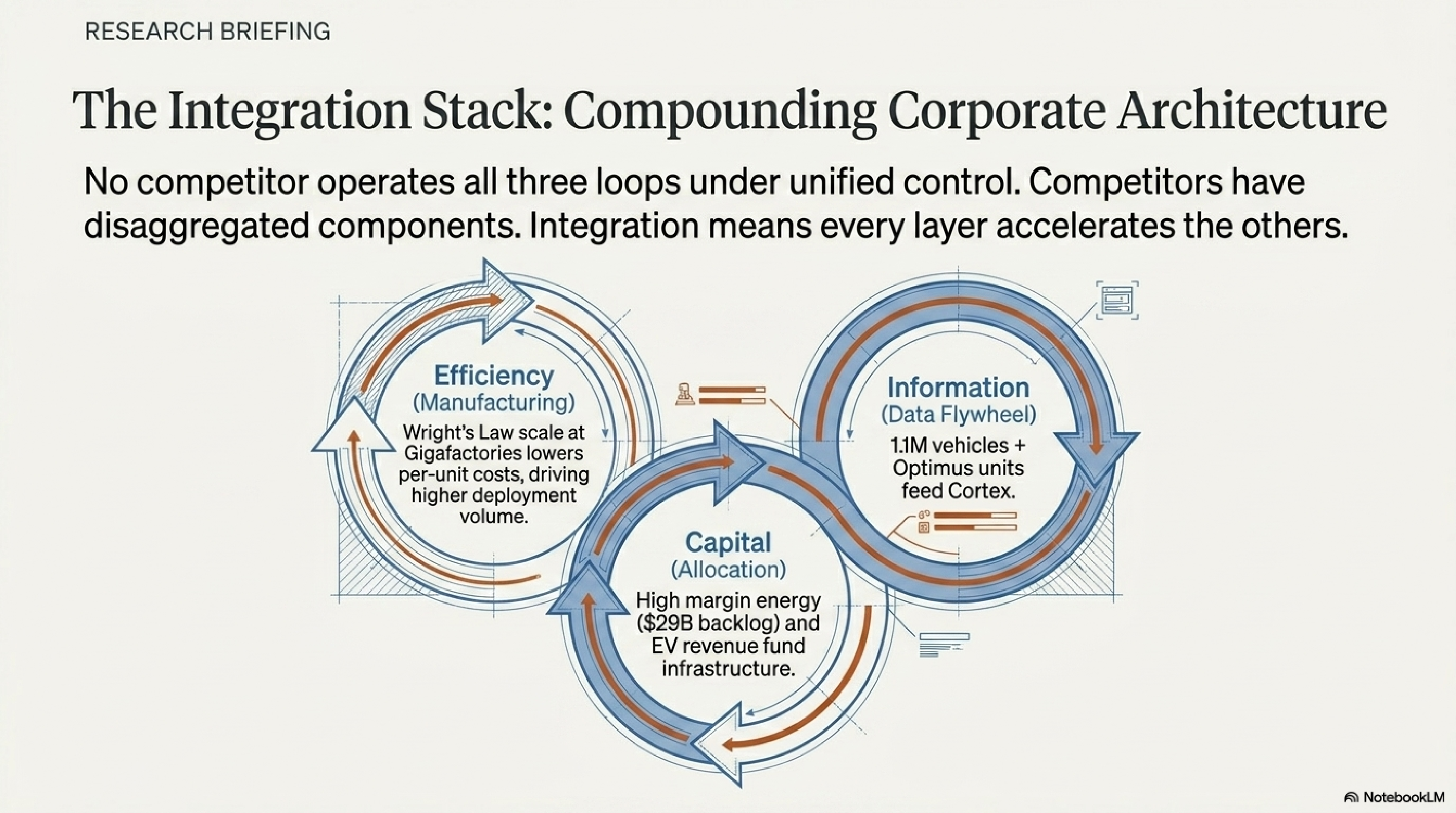

The Integration Stack: Compounding Corporate Architecture

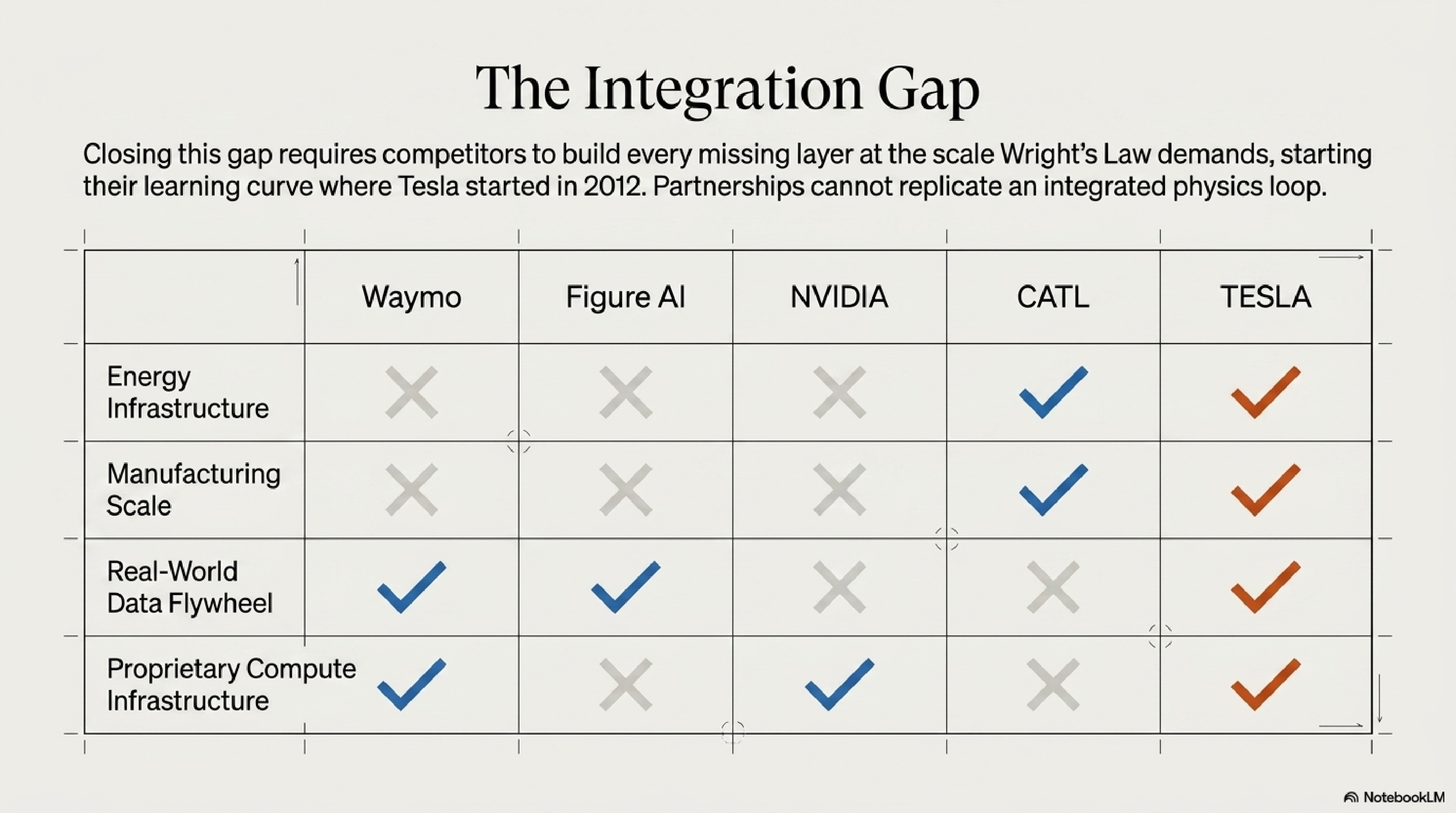

No competitor operates all three loops under unified control. Competitors hold disaggregated components — NVIDIA holds compute, Waymo holds a data flywheel, CATL holds manufacturing scale. Integration means every layer accelerates the others. The three loops run simultaneously inside one balance sheet.

The Efficiency loop: Wright's Law scale at Gigafactories lowers per-unit costs, driving higher deployment volume. The Information loop: 1.1 million vehicles plus Optimus units feed Cortex with real-world data, improving model accuracy and deployment safety. The Capital loop: high-margin energy revenue ($29B backlog, 39.5% gross margin) and EV revenue fund infrastructure that keeps both other loops running.

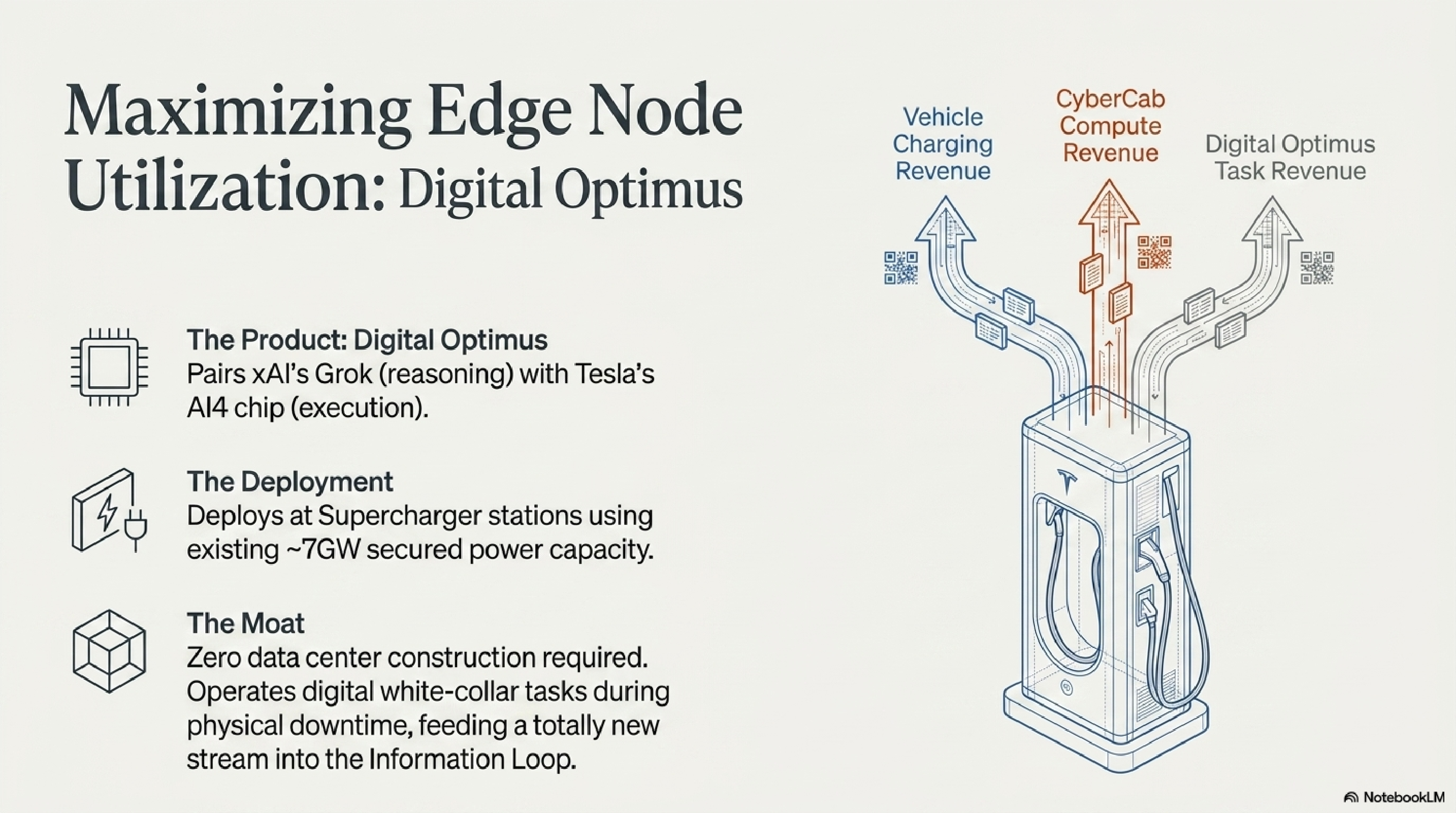

Maximizing edge node utilization: Digital Optimus

Digital Optimus pairs xAI's Grok reasoning model with Tesla's AI4 execution chip. Deployment runs at Supercharger stations using the existing ~7GW of secured power capacity. Zero data center construction required. The unit operates during physical vehicle downtime — the charging interval — running digital white-collar tasks that feed the Information loop with a new revenue stream. Vehicle charging revenue, CyberCab compute revenue, and Digital Optimus task revenue converge at the same hardware node.

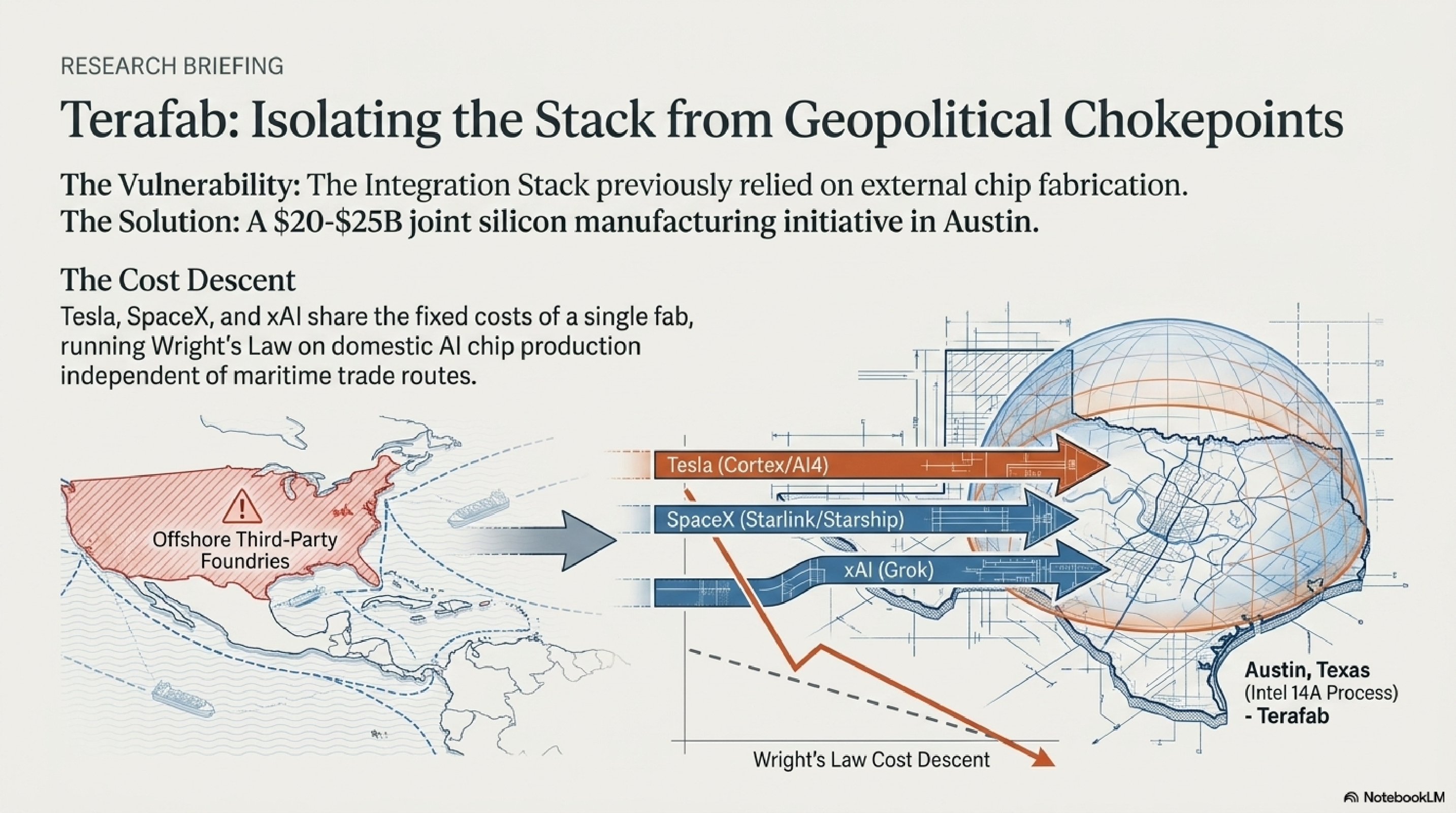

Terafab: isolating the stack from geopolitical chokepoints

The Integration Stack previously relied on external chip fabrication through offshore third-party foundries — a maritime supply chain vulnerability the 2026 Crucible exposed directly. Terafab addresses the vulnerability: a $20–25 billion joint silicon manufacturing initiative in Austin, Texas, running on the Intel I4A process. Tesla, SpaceX, and xAI share the fixed costs of a single fab, running Wright's Law on domestic AI chip production independent of maritime trade routes. Each company contributes its own chip design — Cortex/AI4, Starlink/Starship, Grok — and shares the learning curve that drives all three cost descents simultaneously.

The Integration Gap

Closing the gap requires competitors to build every missing layer at the scale Wright's Law demands, starting their learning curve where Tesla started in 2012. Partnerships cannot replicate an integrated physics loop. A company that licenses a data flywheel does not inherit the manufacturing scale that generates the deployment volume. A company that builds compute infrastructure without the real-world deployment base generates no data to train on. The gap compounds in Tesla's favor with every quarter of deployment.

Geopolitical Validation of the Cost Curves

Geopolitics did not build the Integration Stack. Market economics and Wright's Law built the stack. Geopolitical stress simply reveals the strategic value the math already created. The validation timeline runs across eleven years of independent decisions by competing geopolitical actors — each decision accelerating the cost descent regardless of the actor's intention.

May 2015: China declares industrial dominance strategy in solar and battery manufacturing. February 2022: Russia's invasion exposes European fossil fuel dependency. August 2022: the US Inflation Reduction Act passes as industrial competition against Chinese clean energy dominance. January 2026: Texas bans CATL batteries on national security grounds — the domestic Megapack loop closes. 2027 projection: LG LFP Michigan plant closes the domestic Megapack loop completely.

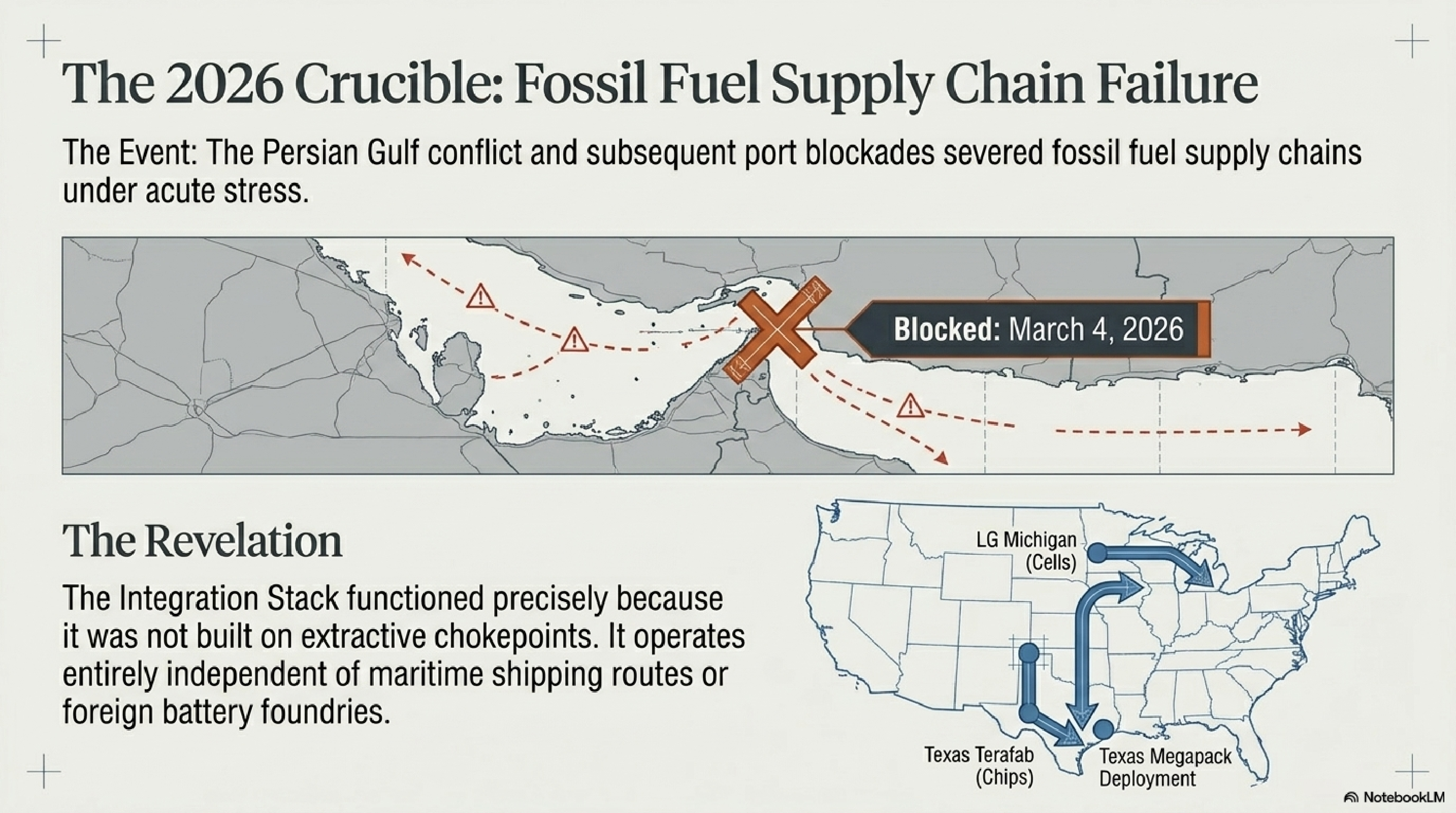

The 2026 Crucible: fossil fuel supply chain failure under acute stress

The Persian Gulf conflict and subsequent port blockades in March 2026 severed fossil fuel supply chains under acute geopolitical stress. The Integration Stack functioned precisely because the stack does not depend on extractive chokepoints. The stack operates independent of maritime shipping routes and foreign battery foundries. LG Michigan supplies cells. Texas Terafab supplies chips. Texas Megapack deployment runs from domestic production. The 2026 Crucible did not create the stack's strategic value — the Crucible revealed the value that Wright's Law had already built.

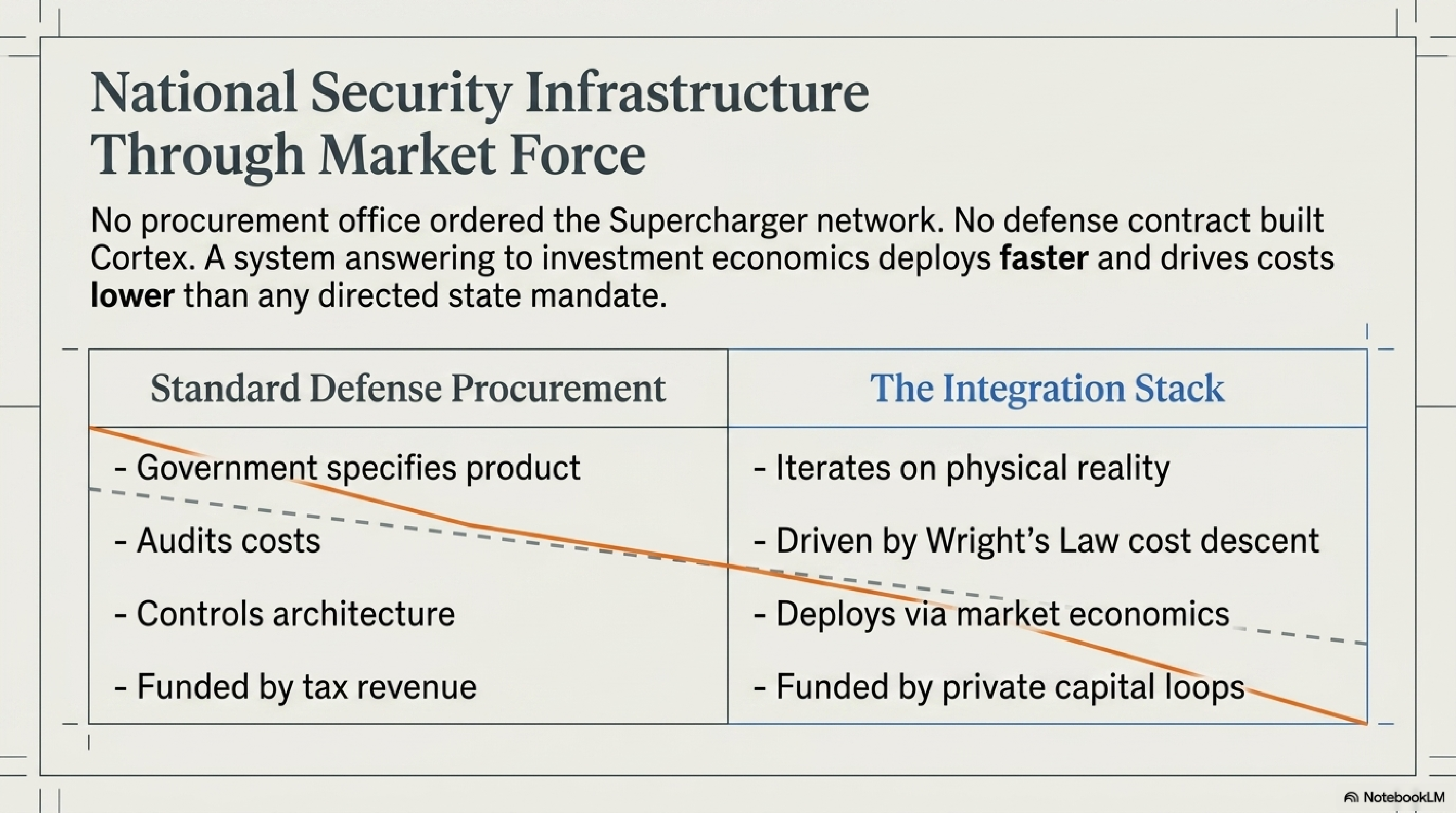

National Security Infrastructure Through Market Force

No procurement office ordered the Supercharger network. No defense contract built Cortex. A system answering to investment economics deploys faster and drives costs lower than any directed state mandate. The comparison with standard defense procurement makes the structural difference explicit: government specifies product, audits costs, controls architecture, and funds through tax revenue. The Integration Stack iterates on physical reality, runs Wright's Law cost descent, deploys via market economics, and funds through private capital loops.

The United States cannot run national energy security through a single corporate architecture. The security imperative generates demand for domestic replication. Strategic capital does not price the Integration Stack as a consumer technology company. Strategic capital prices the stack as the master model for a new class of sovereign infrastructure — the Abundance Economy's operating system, built through market force rather than state mandate.

The Abundance Economy is mathematically inescapable. The Integration Stack is its operating system.